How concentrated are Public VC portfolios in SpaceX, OpenAI and Anthropic?

And what happens after these companies list?

The frenzy around private market AI has reached fever pitch.

Public VCs (“PVCs”, such as DXYZ, VCX and RVI) have all benefited from this clamor for access to the major three private AI players (SpaceX, OpenAI and Anthropic). A momentum trade is well underway, where each PVC could potentially be considered a proxy stock for the underlying AI companies.

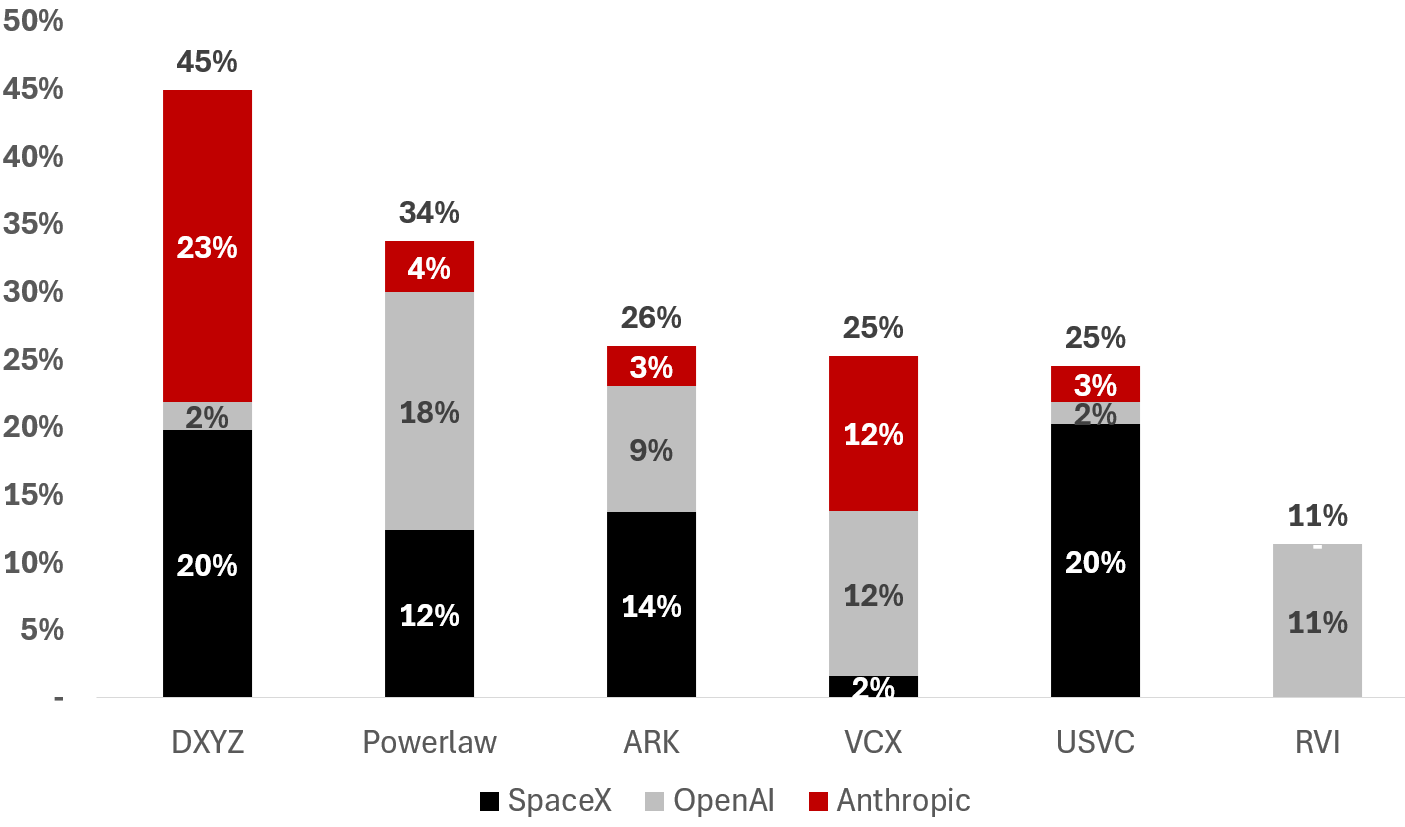

Figure 1 shows the percentage of NAV for each PVC in the big three private AI companies (based on latest public filings).

Figure 1. % of NAV in top three private AI companies (per latest public filings)

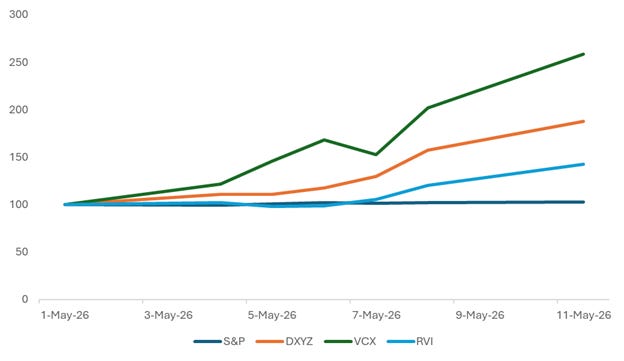

The market response to this portfolio construction has been strong. Since 1 May 2026 alone (just 10 days ago), VCX (with a slim float) has risen over 150%, while DXYZ is up 88% and RVI is up 42%. The S&P (which itself is on fire) is up a measly 3%. See Figure 2.

Figure 2 Select PVC share prices vs S&P 500 from 1 May 2026 (re-based to 100)

Each PVC is trading at a significant premium to NAV as retail investors seek ownership of these companies prior to their respective rumored listings. These three PVCs are trading at an average share price to NAV multiple of 5.9x (premium to NAV of 490%).

Figure 3 Share price to NAV multiple for select PVCs since listing (as at 11 May)

multiples for various cryptocurrencies, including DXYZ, VCX, and RVI, over a period leading up to May 2026.

AI-generated content may be incorrect.")

What happens after the AI companies go public?

The key question is whether these premiums are sustainable once the underlying assets themselves become publicly traded. Are PVCs permanent access platforms deserving structural premia, or temporary scarcity vehicles whose premiums disappear once the underlying assets become liquid?

You could argue that each of these private AI assets are experiencing such strong revenue growth that each continues to be undervalued. Anthropic is approaching a valuation in the secondary markets of $1 trillion, based on spectacular reported revenue growth to $30bn annualized run-rate by April 2026. Revenue guidance continues to be revised upwards.

Under this framework, it may make sense for PVCs to retain positions post listing rather than immediately distributing or exiting them.

The mandates of the PVCs are primarily focused on private assets, but the CEOs of DXYZ and VCX respectively have publicly stated that they have some discretion to hold on to public assets:

“Our mandate is to provide exposure to what we believe to be 100 of the top venture-backed *private* technology companies. That said, especially as we’ll own larger positions in some companies, we maintain discretion to manage this. With that in mind, as portfolio companies go public we generally hold on to their shares and systematically divest over time.”

The private companies want long-term holders. Investors want us giving them exposure to private tech, which otherwise they can’t usually get access to. After ServiceTitan went public, we sold the majority of our shares.

Nevertheless, there is a strong argument that the scarcity premium currently embedded in these vehicles could compress materially once investors are able to access the underlying assets directly in public markets.

Retail investors will simply be able to buy SpaceX in the open market, so why do you need the PVC wrapper? And why pay a premium in the PVC wrapper?

The obvious counterargument is that PVCs could continue to command premiums if investors believe they will repeatedly gain access to future generations of high demand private companies prior to IPO. In that sense, the vehicles themselves become perpetual access platforms rather than simple holding companies.

Indeed, the IPOs of the three AI companies will generate significant liquidity for the PVCs who will then be looking to reinvest any undistributed cash into the next generation of power law companies.

Concluding thoughts: SPV ownership

One additional consideration is the growing use of SPV structures to gain exposure to highly competitive private deals. In many cases, PVC exposure to companies such as SpaceX, OpenAI and Anthropic is indirect, layered through various SPV arrangements.

This structure is increasingly attracting scrutiny, particularly as leading private companies seek tighter control over their cap tables and secondary trading activity.

Anthropic today updated their policy to address this exact point:

Any sale or transfer of Anthropic stock, or any interest in Anthropic stock, that has not been approved by our Board of Directors is void and will not be recognized on our books and records.

None of this necessarily implies wrongdoing or misrepresentation by PVCs. However, it does highlight the complexity of indirect ownership structures in late stage private markets. Investors may ultimately discover that their economic exposure differs materially from their assumptions regarding direct ownership, transferability, governance rights or liquidity.

The eventual transition of these assets into public markets will therefore be an important test, not only for the valuations of OpenAI, Anthropic and SpaceX themselves, but also for the durability of the premium investors are currently willing to pay for private market access (especially investments held in opaque SPV structures).

oh thanks for the article, this was a really sharp read. the wrapper math after IPO is the part most retail isn't pricing in yet