Public VC fees

Benchmarking fees across comparable funds

In this post, we compare fees across different public venture capital managers (“PVCs”) based on published prospectuses.

Each fund prospectus has a standardized section on fees & expenses which allows for a read across for each fund.1

The average management fee is 2.0%, plus an additional ~1.5% of other fees, bringing the total average fee load to ~3.5%. This is higher than the standard 2/20 private VC model, although note that closed-end funds cannot have carry or incentive structures.

PVC managers have launched first generation products. It is early in this asset class. We should expect fee compression as the products mature.

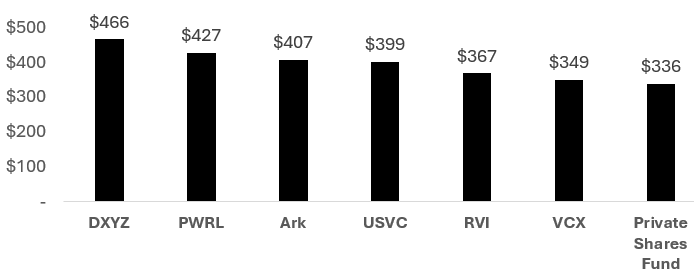

Expected cumulative fees after 10 years

Each prospectus includes a table with a hypothetical example which assumes a $1,000 is invested for a 5% annual return. It is this table we have used to create Figure 1 to consider the expected cumulative fees per manager over 10 years.

Figure 1. Expected cumulative fees over 10 years from a $1,000 investment

Source: public filings based on standard hypothetical example which assumes $1,000 invested over 10 years and 5% annual return

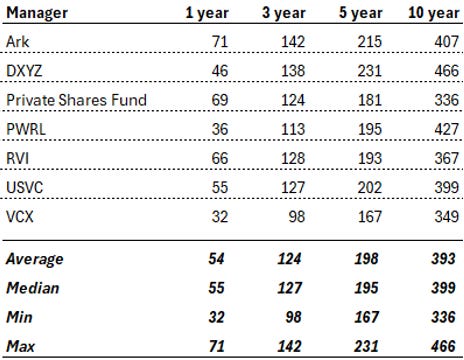

This chart is based on the 10 year data from Figure 2, which also shows the cumulative fees per manager for 1 year, 3 years, and 5 years.

Figure 2. Cumulative fees over different time periods for $1,000 investment ($)

Source: public filings based on standard hypothetical example which assumes $1,000 invested over 10 years and 5% annual return

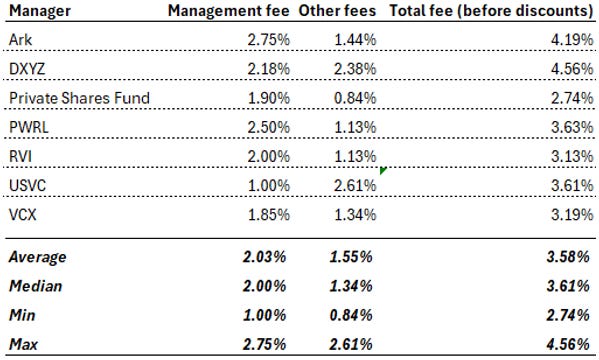

Fee breakdown

The annual fee tables in the prospectuses consist of management fees and other fees. Figure 3 shows the total annual fees for each manager from their prospectuses.

Figure 3. Annual fees & expenses per manager

This table is on a gross basis. Some managers are currently offering discounts (with USVC currently offering a 1.11% discount to bring the net fee down to 2.50% per year).

The table above does take into account any management fees in underlying vehicles (“Acquired Fund Fees & Expenses” in the prospectuses). USVC, for example, is an LP in emerging managers, so needs to take into account the 2% management fees for the VC funds.

However, this fee load does not take into account the multi-layer SPV carry load. Any carry is presumably netted from exit proceeds before distributed to the PVC vehicles.

Note that these US closed-end funds do not have carry structures themselves (even if carry is paid in the underlying SPVs). This is a major structural & regulatory difference compared to private VC funds with 2/20 models.

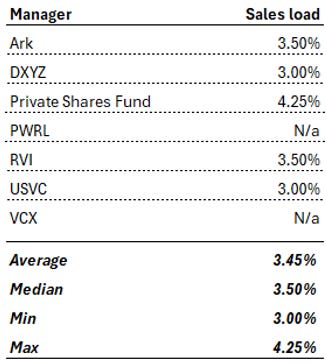

Each prospectus also splits out any sales load for raising capital for these funds. The average is ~3.5%. See Figure 4. This sales load is in addition to the ongoing fees in Figure 3.

Figure 4. Sales load per manager

Concluding thoughts

It is the first innings of PVCs. Many of these funds are still sub-scale and gathering assets at pace. DXYZ, for example, started with NAV of <$50m in 2024 and has raised ~$250m per quarter for the last two quarters.

Nevertheless, the optics of fees in the 3-4% range are not good, especially as these are essentially passive funds.

If we look at analogous asset classes, we should anticipate fees to compress with greater product development and greater competition.

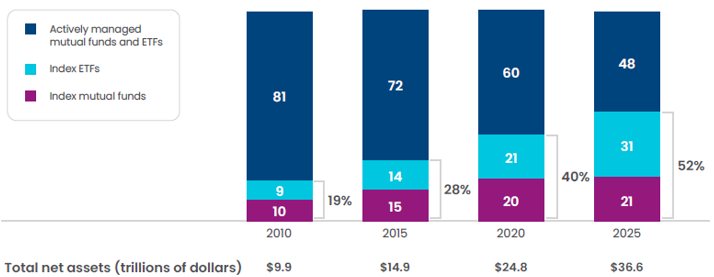

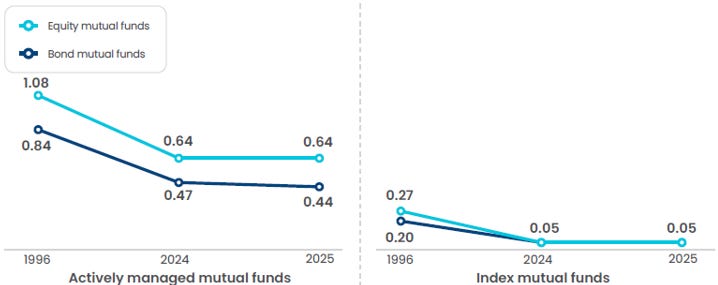

The story of the public markets in the last sixty years is really the triumph of passive over active. Passive AUM is now greater than active AUM (Figure 6). This is in part due to performance and in part due to fees. According to SPIVA, 90% of active US large-cap managers underperformed the S&P 500 over the last 15 years. And passive funds outperformed with substantially lower fees (Figure 7).

Figure 6 % of long-term funds’ total net assets

Source: Investment Company Institute

Figure 7. Average expense ratios for active & index mutual funds

Source: Investment Company Institute, Lipper & Morningstar

The current PVCs do not claim to be indexes, as they tend to be more concentrated bets on a handful of late stage private companies. So the comparison with index mutual funds is perhaps somewhat unfair.

Nevertheless, the mutual fund story is illustrative of a broader trend.

In the longer term, we should anticipate that fees in private market passive vehicles to mimic public market passive vehicles. This could also have a knock-on effect of lowering active VC manager fees. Fees should compress over time.