Why some public VCs trade above NAV

We are in the midst of a flurry of new listings for Public Venture Capital (“PVC”) funds. Fundrise & Robinhood Ventures are already trading. Powerlaw and RiverNorth are waiting in the wings. More groups are in prep mode.

The current PVC products are trading well, typically above Net Asset Value. This flies in the face of received wisdom which until recently accepted that listed entities with private assets trade at discounts to NAV.

And in many ways the premia/discount to NAV debate is a red herring to the core question of whether NAV itself is growing. It is this NAV growth that is core to SignalRank’s own model (given our focus on Series Bs, not pre-IPO stocks), not the premium/discount to NAV.

Nevertheless, what are the key factors in driving share price to trade at a premium to NAV? And how do these impact the current stable of PVCs?

Factors driving share price

Public funds of private assets typically trade at a discount to NAV. The main reasons are as follows:

Liquidity discount: investors apply a discount to a portfolio due to the fact that the underlying assets (private companies, real estate, some crypto) cannot be instantly sold. The more illiquid the assets, the greater the discount.

Valuation skepticism: internal valuations are set by managers, leading investors to question a NAV number that hasn’t been stress-tested in an actual sale.

Higher fees: managers of private assets typically charge higher fees (and carry) than their public market colleagues, which has a negative impact on NAV.

Thin demand: trading volumes in these assets tend to be somewhat low, leading to greater bid/ask spreads.

And yet. The newer models of PVCs are overcoming these factors to trade at premia to NAV, not discounts. This is primarily due to:

Brand awareness: portfolios with assets such as OpenAI & SpaceX benefit from high retail awareness of the underlying assets.

Asset scarcity: investors pay to access quality assets which are unavailable elsewhere, such as Anthropic.

Thin float: PVCs operating within lock-up periods have smaller floats which will artificially impact the movement of shares, given limited access to the shares.

Some secondary components also come into play such as the listing location (with US public investors valuing growth more than in Europe), market sentiment (especially the AI frenzy today), first mover advantage (as the market does not understand PVCs yet) and portfolio concentration (with some PVCs being so concentrated as to be proxies for single assets).

But it is worth noting that these premia historically tend to compress, as new supply eventually meets demands (rights issues, competing vehicles, eventual IPOs of the underlying companies that remove the exclusivity premium).

Again, NAV growth itself should be more important than premia/discounts to NAV.

Premia/discount to NAV for existing PVCs

Listed VCs are not a new phenomenon in Europe. Government / public-funded capital remains the largest source of LP capital in Europe. It has historically been challenging for non-Tier 1 European managers to raise commercial capital, forcing some to resort to the public markets as a source of capital.

These platforms have typically underperformed. This is perhaps of no surprise, given these GPs’ inability to access generational companies, combined with thin European capital markets and a conservative European public market investor base.

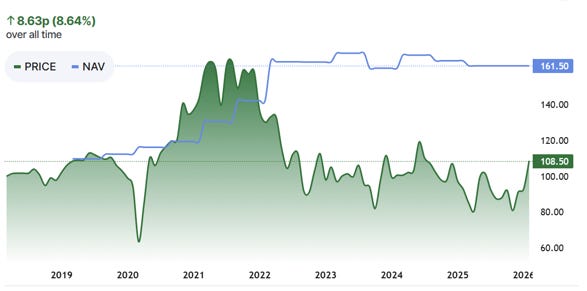

Covid-mania led Molten Ventures (Figure 1) and Augmentum (Figure 2), which are two listed VCs in the UK, to briefly trade above NAV. The norm today is more like a 35%+ discount to NAV.

Figure 1. Molten Ventures share price & NAV evolution since 2016

Source: Hargreaves Lansdown

Figure 2. Augmentum’s share price & NAV evolution since 2018

Source: Hargreaves Lansdown

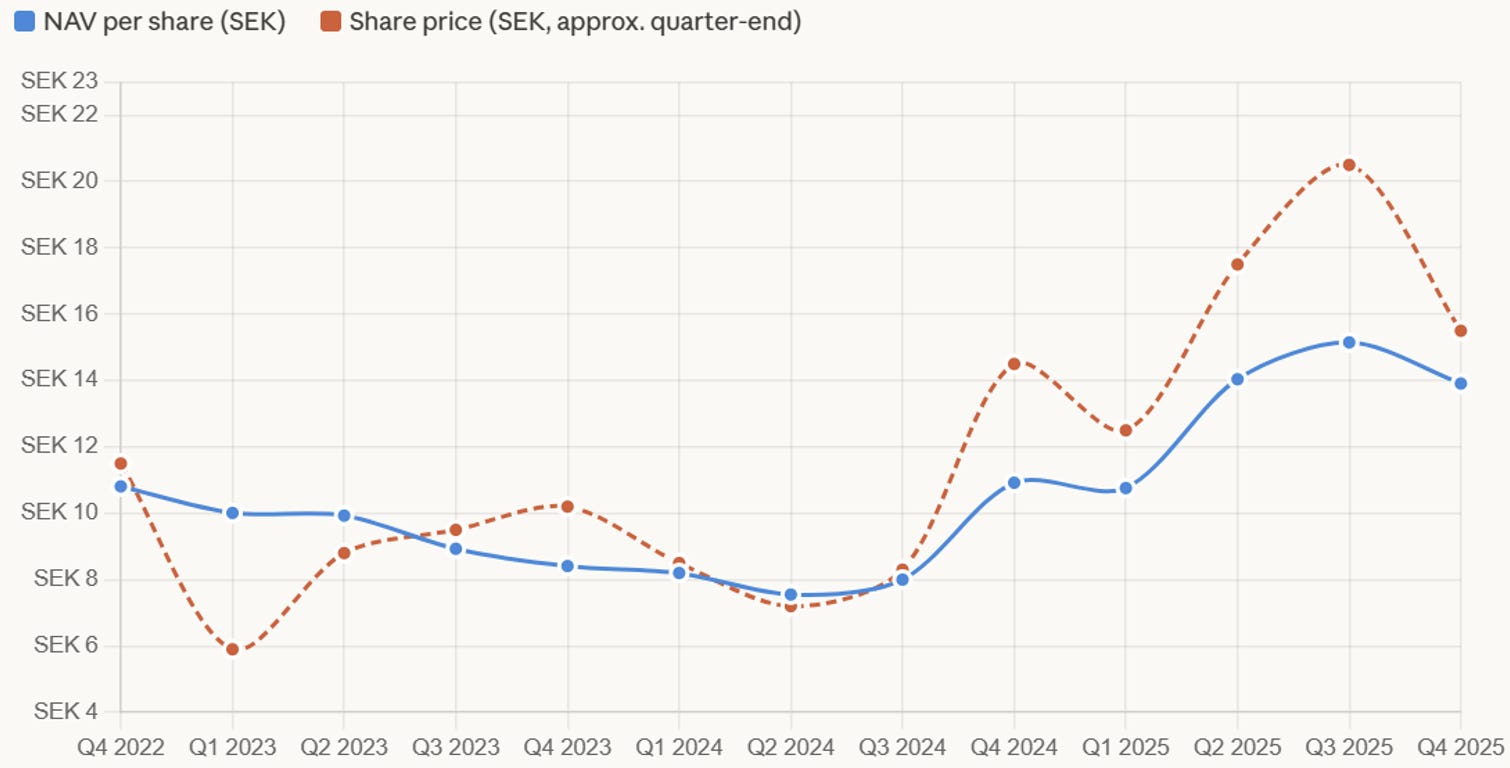

It is not all bad news in Europe. Flat Capital, run by Klarna CEO (Sebastian Siemiatkowski), has significant positions in OpenAI as well as Klarna itself. This has led Flat Capital to trade at a premium to NAV since Q3 2024 (Figure 3).

Figure 3. Flat Capital’s share price & NAV evolution since 2022

Source: Claude

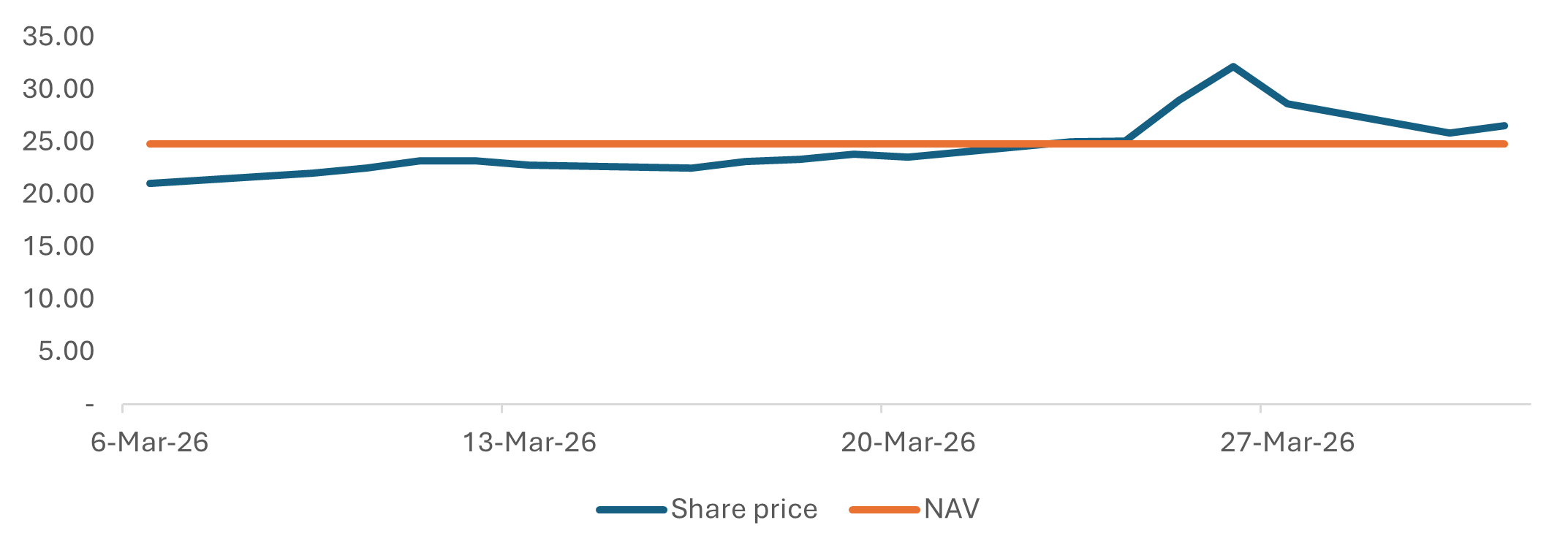

Turning to the more recent US PVCs, DXYZ has consistently traded at a premium to NAV (Figure 4) since listing in 2024.

This spiked at 20x+ at the initial listing and jumped again with Trump’s 2024 re-election (which benefited SpaceX which was 50%+ of the portfolio at the time), before stabilizing at an average of 380% premium to NAV for 2025. This subsequently reduced further as DXYZ raised almost $250m in Q4 2025, bringing the average premium to NAV for 2026 to 40%.

Figure 4. DXYZ’s share price & NAV evolution since listing

Source: Yahoo Finance

There is less history for Robinhood Ventures and Fundrise which both listed in Q1 2026.

Robinhood Ventures (RVI), underwritten by Goldman Sachs, has seen a more stable trading pattern (Figure 5). The lack of a initial pop probably speaks to a portfolio that is underweight AI, focused more on winners from the prior cycle and consumer-facing products that will appeal to their 27m account holders. The success of the Fundrise listing did drag the RVI share price above NAV, and RVI currently trades at a 7% premium to NAV.

Figure 5. Robinhood Ventures’ share price & NAV evolution since listing

Source: Yahoo Finance

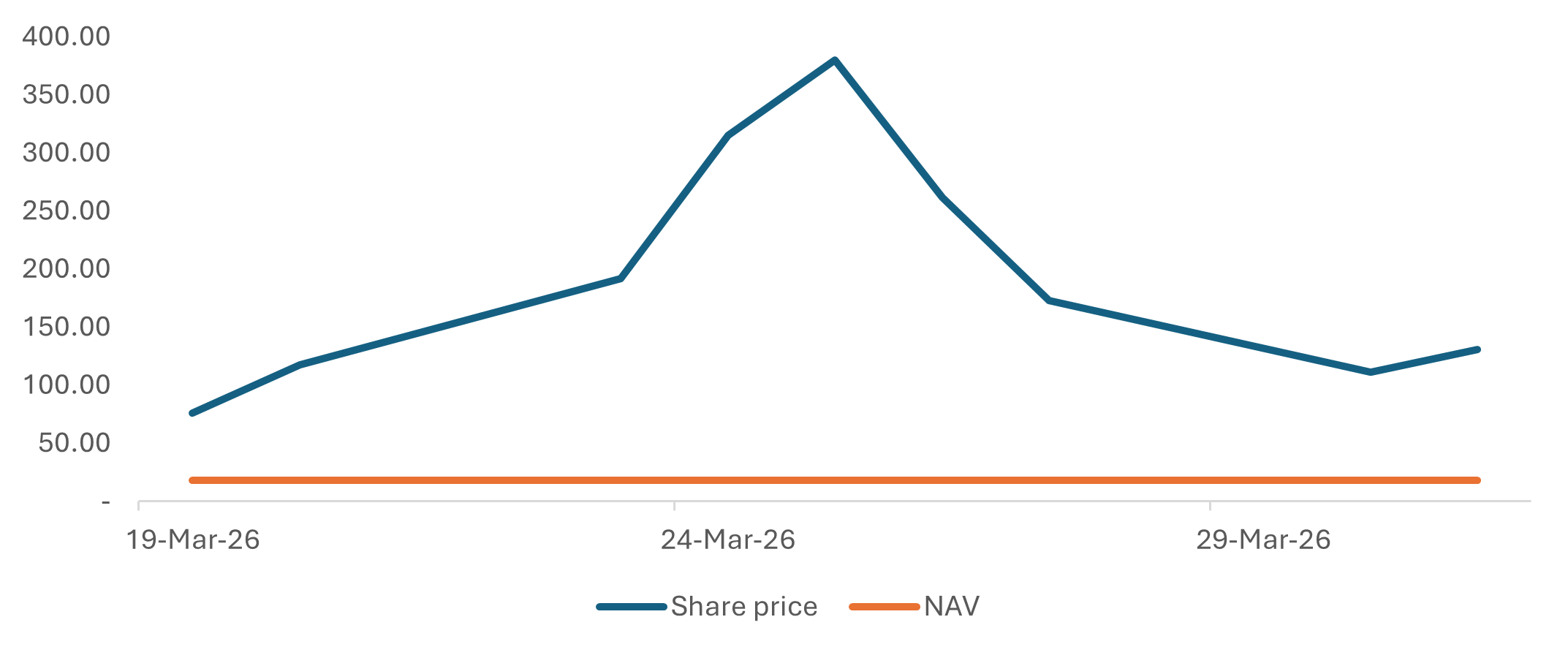

By contrast, Fundrise’s share price evolution is much more in-line with DXYZ (Figure 6). The combination of a portfolio with prized assets and a very thin float has led VCX to trade wildly in initial sessions. Current share price as at 3/31/26 is above 600% premium to NAV.

Figure 6. Fundrise’s VCX share price & NAV evolution since listing

Source: Yahoo Finance

Closing thoughts

We have previously written about why fund structure matters. In the US, the closed-end fund model allows the share price to diverge from NAV (like DXYZ), while other structures, including the interval fund structure that ARK Ventures selected, are tied exactly to NAV.

This led to a public spat between DXYZ’s CEO, Sohail Prasad, and ARK’s Cathie Wood.

In the long term, this is noise. As more and more PVCs come to market offering similar products, the premia to NAV will likely compress, unless tied directly to expected NV growth.

Indeed, what will differentiate managers is those whose products can deliver consistent NAV growth and those who cannot.

We have a small cap PVC on the Bulgarian Stock Exchange (Eleven Capital) and we have experienced similar trend of initial premium compressing to a discount around 20%. But we have always claimed and have been focused on NAV growth.