State of Series B ecosystem

H1 2026 update

We are pleased to share here our H1 2026 report on the state of the Series B ecosystem.

The SignalRank Index is designed to reflect top Series Bs in terms of MOIC potential. As such, understanding the Series B ecosystem is critical to our business model.

In this post, we will consider key trends in the Series B ecosystem in H1 2026.

We hope you enjoy the report.

Executive summary

Series B resurgence: the number & size of Series Bs is almost 20% higher than in H1 2025.

Bifurcated market: most of the 2026 Series Bs we have seen from our seed partner network are at $150-200m pre-money. A tiny subset of AI rocket ships (which are attracting all the attention) are raising at $1bn+ pre-money at Series B.

Key sectors: AI, defense, FinTech and robotics are the sectors driving the highest quality Series Bs. The US continues to be the dominant market for Series Bs.

Series C graduation: Series Cs are also starting to pick up, albeit still somewhat muted relative to pre-Covid period. Ditto IPOs.

SignalRank operating at scale: SignalRank invested in 16 Series Bs (of which 11 have been announced) in H1 2026, making SignalRank one of the most active Series B investors globally. We are on track to invest in 30 Series Bs this year.

1. Aggregate Series B data

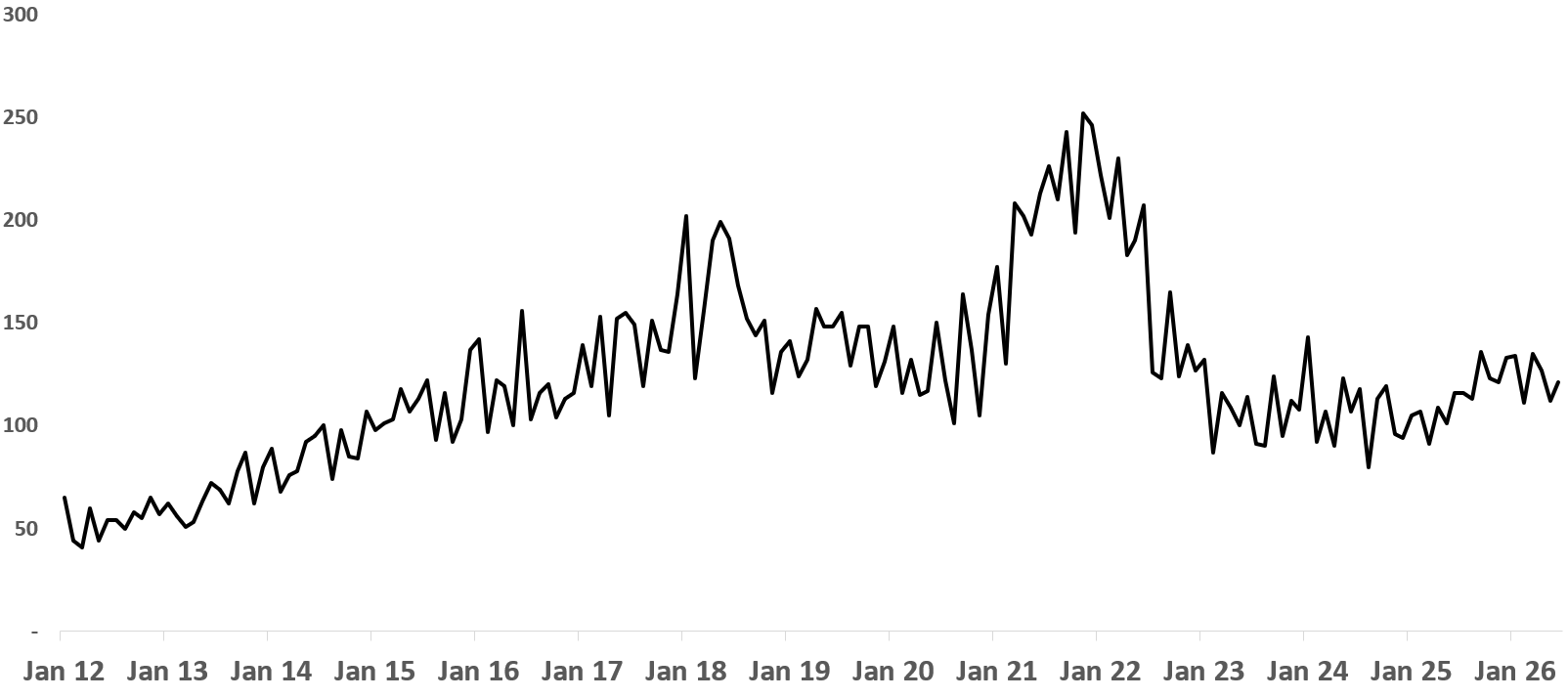

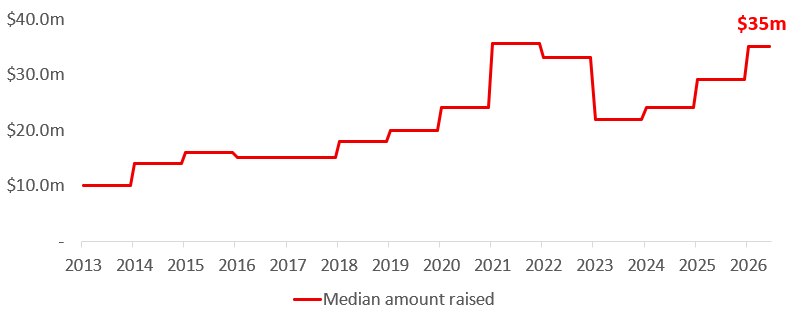

The AI boom is driving growth at Series Bs. We are seeing a rise in the monthly number of Series Bs (Figure 1), as well as in the median round size (Figure 2).

Figure 1. # of Series Bs globally per month (2012-26)

Figure 2. Median Series B round size (2012-26, $m, Crunchbase data)

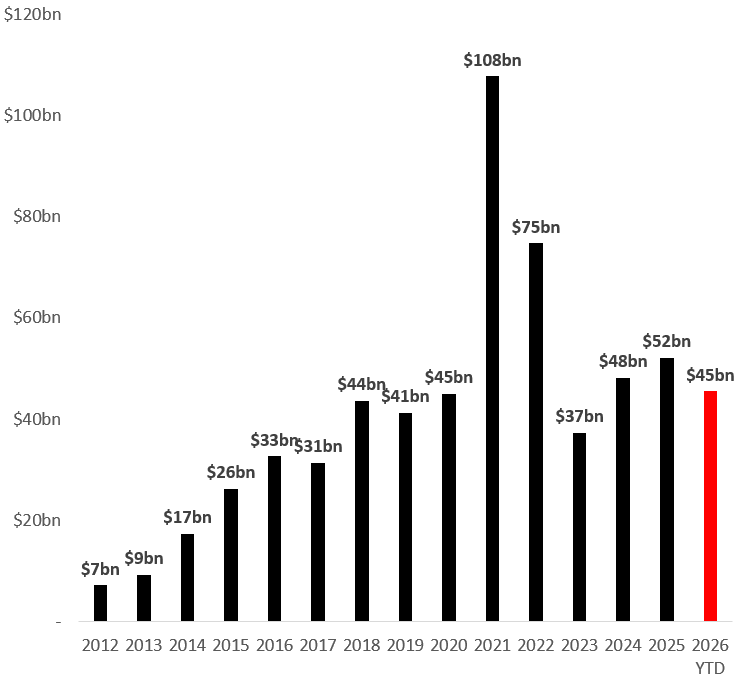

As a result, the aggregate capital invested into Series B has increased (Figure 3). Even without the $12bn Series B raised by Prometheus this year, the amount raised is on course to surpass 2025 levels easily.

Figure 3. Aggregate capital raised at Series B (2012-26 YTD, Crunchbase data)

2. Bifurcated market

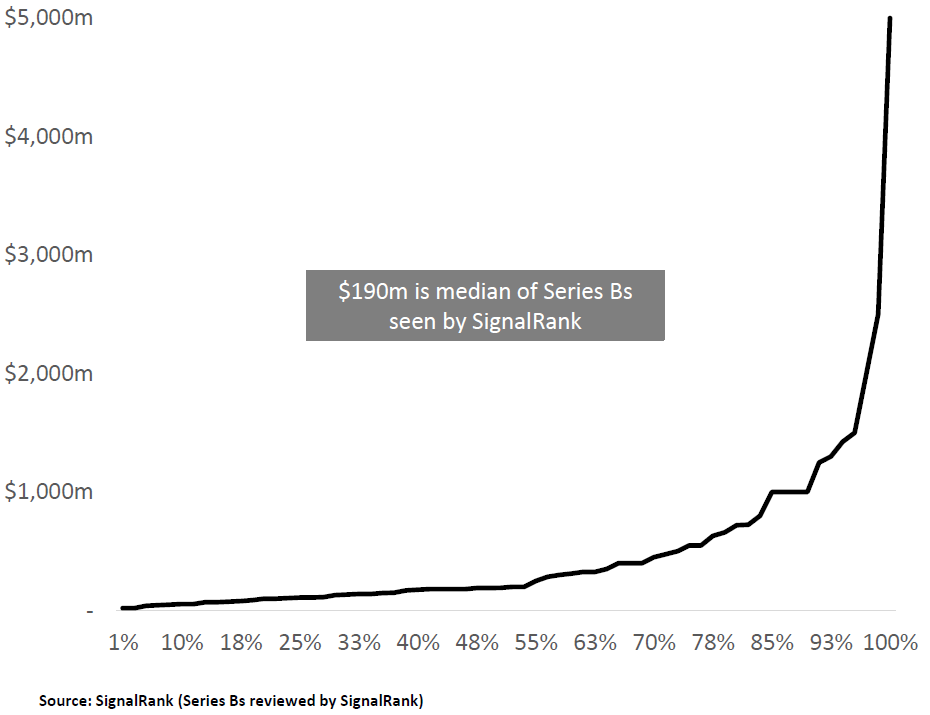

The aggregate data masks a highly divided market: most companies are raising Series Bs at less than $200m pre. A tiny subset of AI companies is raising at $1bn+.

Figures 4 shows the distribution of pre-money valuations for all Series Bs seen by SignalRank in 2026 (shared by 89 unique seed partners).

Figure 4. 2026 Series B distribution of pre-money valuations ($m)

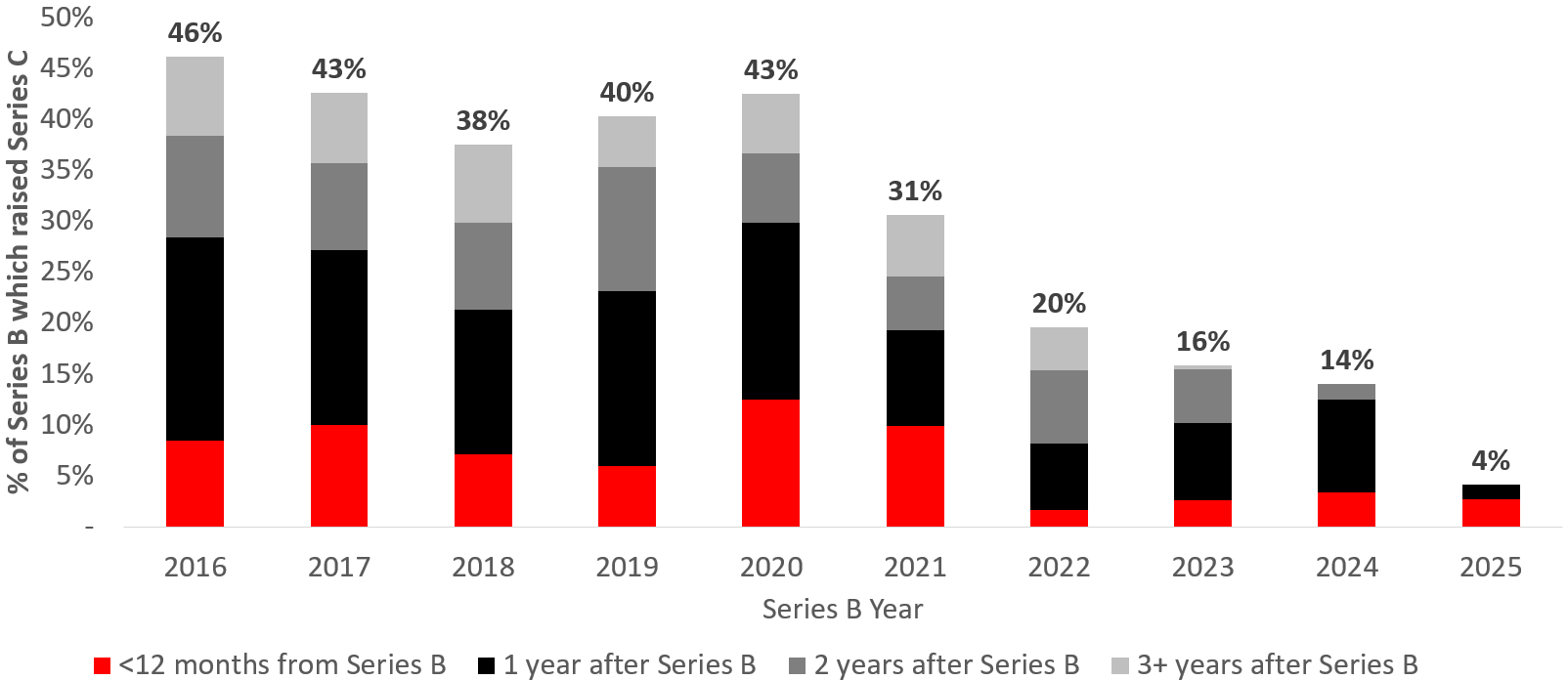

3. Series B conversion: Series C market data

The Series C market is also growing again. Yet it remains subdued relative to pre-Covid levels. Only ~12% of Series Bs are raising a Series C within 24 months (compared to ~30% prior to Covid, Figure 5).

Figure 5. Series B conversion: time to raise a Series C (2016-25)

3. Most active investors

Y Combinator was the most active Series B investor in H1 2026 with 16 announced rounds, followed by Accel and Sequoia Capital.

Figure 6. Top 10 most active Series B investors in H1 2026 (announced rounds)

4. SignalRank performance

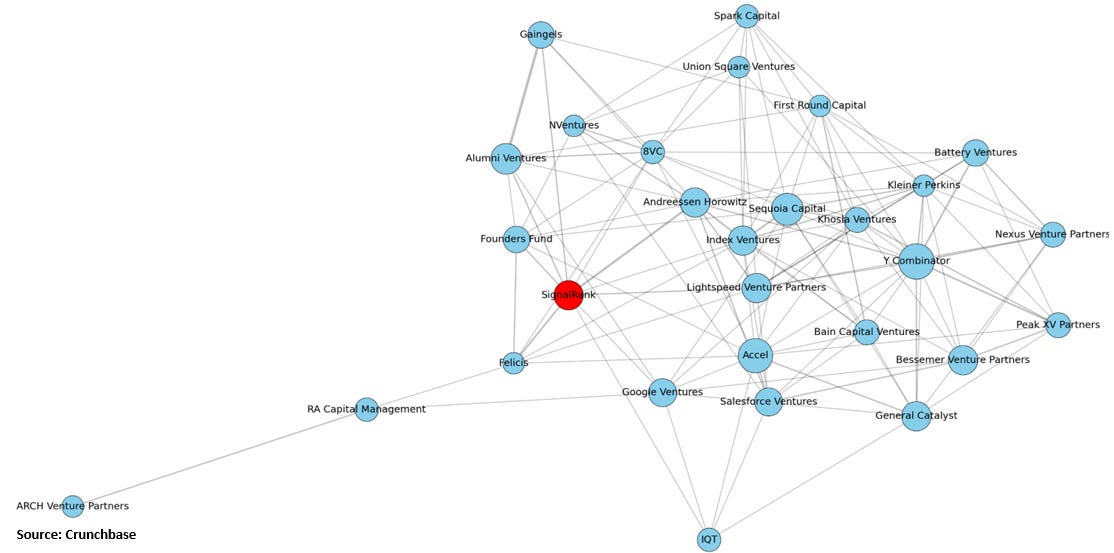

SignalRank continues to have high network centrality within the Series B ecosystem, demonstrating that our systematic approach is delivering consistent access to companies backed by high quality active investors (Figure 7).

Figure 7. All investors with 5+ 2026 Series B investments, with edges showing 2+ co-investments

Figure 8. SignalRank completed 16 investments in H1 2026

SignalRank completed 16 investments in H1 2026 (Figure 8). Of these five are ranked in the top 20 for all Series Bs this year (per our methodology, Figure 9).

Figure 9. Top 20 ranked Series Bs in H1 2026

We are accessing high quality Series Bs at scale. We are on track to make 30 qualifying investments in 2026, delivering on the promise of an index-like Series B investment product.