The $106 Billion Secondaries Market: Secondary Exits Are Now Structural

Robinhood, Public Venture Capital, and Packaging Secondary Sales for Retail Investors

This article was written in collaboration with my OpenClaw Agent. It was not written by it. I take all responsibility for the content. Just FYI.

PitchBook published its 2025 Annual US VC Secondary Market Watch this week. The headline number: $106.3 billion traded through US venture secondaries in 2025. That figure deserves context, and scrutiny. It accompanies the Thomasz Tunguz piece from last week.

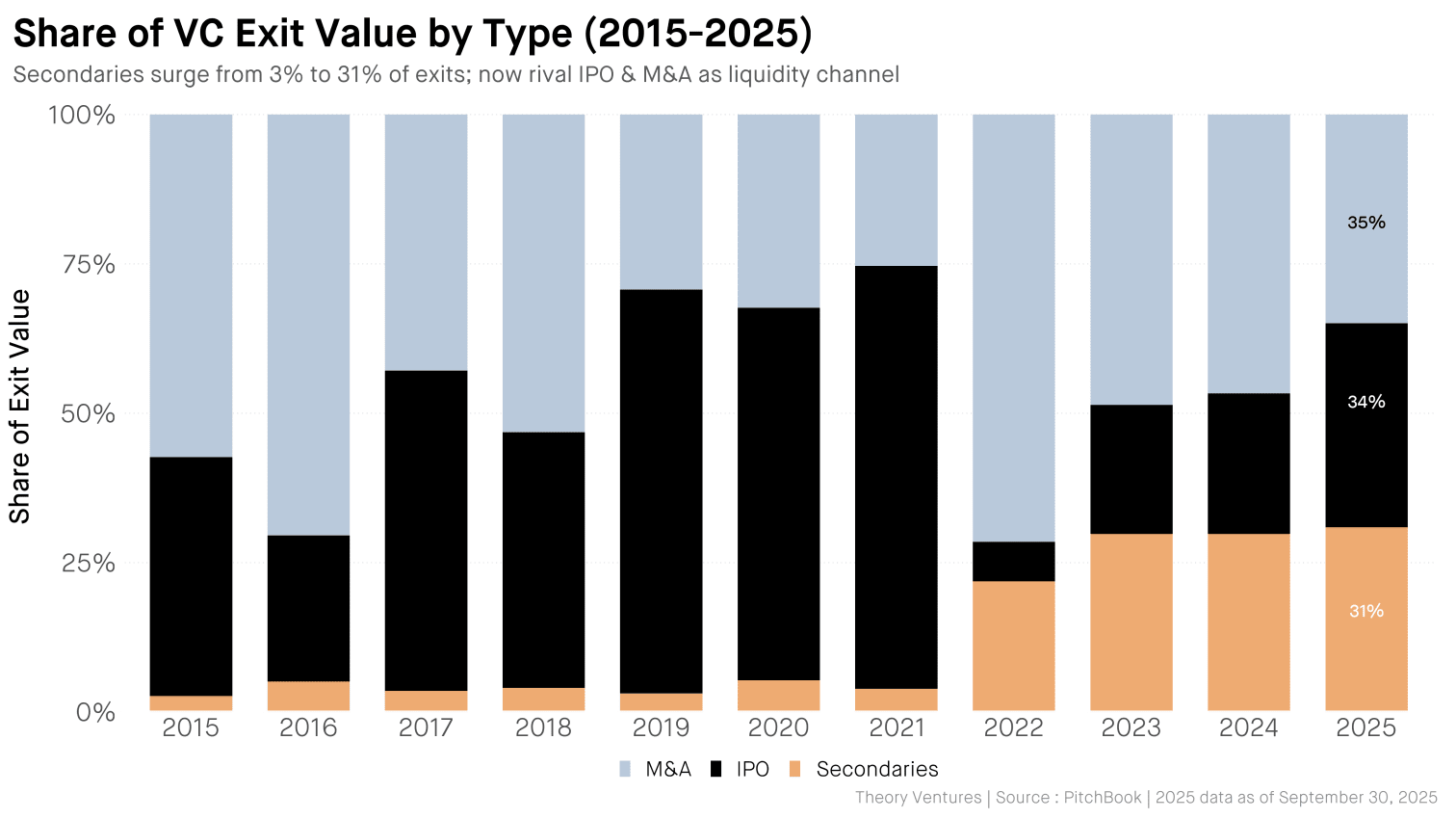

For the first time, venture secondaries are operating at a scale comparable to the two traditional exit channels. Acquisitions delivered $140.7 billion. Public listings produced $119.6 billion. Secondaries - a market that barely registered as an institutional category five years ago - hit $106.3 billion ($91.7B direct + $14.6B GP-led).

As Tunguz acknowledged, this is the third pillar of venture liquidity. It arrived faster than most people expected.

How fast it grew

Annualized direct secondary value went from $50 billion in Q4 2024 to $91.7 billion by Q4 2025. That is an 83% increase in five quarters.

Much of this acceleration was driven by valuation surges at the top end. SpaceX moved from $350 billion to $1.25 trillion in twelve months. OpenAI’s $6.6 billion tender offer alone accounted for 6.2% of annual secondary volume. When a single transaction represents more than 6% of an entire market, that market has a concentration problem.

Concentration

On Hiive, the top 20 startups accounted for 86.4% of secondary trading value in Q4 2025. The top five alone represented 55.6%. SpaceX was the most actively traded name on Augment, representing 12.5% of total platform activity.

The vast majority of the $106 billion secondary market is a handful of mega-cap names trading among sophisticated participants. The long tail - the other 13.6% - is where price discovery is weakest, information asymmetry is greatest, and the risk of adverse selection is highest.

This has direct implications for the emerging Public Venture Capital (PVC) category. The funds now listing on public exchanges - Robinhood Ventures (RVI), Powerlaw (PWRL), Fundrise (VCX), Destiny Tech100 (DXYZ) - are overwhelmingly concentrated in the same top-20 names that dominate secondary volume. They are not diversifying beyond this concentration. They are repackaging it for retail.

$22 billion in acquisitions: who is buying the plumbing

PitchBook documents an institutional buying spree, but the full picture is bigger than their report covers. Over $22 billion in acquisitions in under a decade, the largest financial institutions in the world have been assembling private market infrastructure piece by piece.

Goldman Sachs bought Industry Ventures (~$965M), a secondary fund manager. Morgan Stanley took EquityZen, a secondary marketplace, and Shareworks for equity management. Schwab bought Forge Global (~$660M), another marketplace. JPMorgan acquired Aumni, Global Shares (EUR665M), and First Republic ($10.6B) - cap table intelligence, equity administration, and banking in one sweep. Capital One is acquiring Brex ($5.15B) for startup banking and spend management. Carta has made at least eight acquisitions (Accelex, Capdesk, Sirvatus, SVB Analytics, Tactyc, Vauban, ZenEquity) to own the equity lifecycle from the inside. Piper Sandler launched private markets trading, hiring senior talent from Forge. Nasdaq Private Market partnered with G Squared for priority access to tender offers.

And then there is BlackRock. They acquired Preqin for $3.2 billion and eFront for $1.3 billion. Preqin is the dominant private markets data and analytics provider. eFront is the operating system that alternatives managers use to run their portfolios. Together they give BlackRock the information layer and the operating infrastructure beneath all private markets - the valuations, fund performance benchmarks, deal flow data, and LP intelligence that determine how private assets are priced, compared, and allocated. When the world’s largest allocator of capital owns the definitive pricing and benchmarking infrastructure for private markets, the information advantage that has historically favored private market insiders starts to erode. At least for BlackRock’s institutional clients.

One detail that has not gotten enough attention: several of these acquisitions were European companies. eFront was French. Preqin and Global Shares were British. SVB UK was absorbed in the First Republic deal. American financial giants have been quietly absorbing European-built private market infrastructure.

The common thread across all of it is intermediation: transaction fees, fund management revenues, data subscriptions, and the ability to offer wealth management and institutional clients private market exposure through institutional-grade channels.

What does this mean for PVC funds?

The competitive threat is not deal flow. It is distribution. When Goldman’s wealth advisors can offer clients access to secondary venture through Industry Ventures’ managed funds at NAV, the case for buying DXYZ at a 46% premium or Powerlaw at a 2/20 fee structure gets hard to make. The banks are not competing with PVC funds for SpaceX shares. They are competing for the same investor dollars, and offering a product that is cheaper, better governed, and available without a public market premium.

Tender offers are becoming standard

One of PitchBook’s most consequential findings: company-led tender offers are becoming the default liquidity mechanism. Rather than employees and early investors selling ad hoc on secondary platforms, leading startups are running structured, recurring liquidity programs.

This is healthy. It gives companies control over their cap tables and reduces unauthorized transactions. But it also means the best secondary access is increasingly gated. You get into a tender offer because the company invites you, not because you found a willing seller on a platform.

For PVC funds relying on secondary market access as their core strategy, this is a structural headwind. As companies formalize their liquidity programs, the window for uninvited secondary buyers narrows.

The temporary vacuum ahead

PitchBook projects a decline in secondary volume if SpaceX, OpenAI, and Anthropic go public in 2026, as all three are actively preparing to do. These three companies likely represent 30-40% of current secondary volume, so the short-term impact would be real.

But the medium-term effect is positive. More IPOs mean fresher pricing benchmarks, since public market prices reduce the bid-ask spread problem in private secondaries. They mean an expanded universe - 70 new companies saw their first secondary trade in 2025 ($492M), and IPO exits free up capital to flow toward this broader market. And better price discovery attracts more buyers and sellers, growing the market beyond its current top-20 concentration.

Structural, not cyclical

PitchBook’s core thesis - that secondaries are structural, not cyclical - appears correct. The market grew during the 2021 boom (driven by access demand) and grew again during the 2022-2024 drought (driven by liquidity need). A market that is relevant at both extremes of the cycle is not going away.

The question is not whether secondaries will persist. They will. The question is who benefits from the institutionalization of this market, and who bears the risk.

When Goldman Sachs acquires a secondary fund manager to offer its wealth clients managed venture exposure at NAV, the value proposition is straightforward. When a PVC fund packages similar secondary positions into a retail-facing vehicle trading at a premium to NAV with higher fees and weaker governance, the value proposition for the retail buyer is harder to defend.

US venture secondary dry powder reached $11.8 billion as of June 2025, up 2.8x since 2022. But that still represents only 3.9% of primary venture capital. The secondary market is growing fast, but it is still small relative to the primary market it serves. And 86% of its volume is concentrated in 20 companies.

The structural shift is real. The distribution of its benefits is not yet determined. That is the most important question in the emerging PVC category.

Who benefits?

The infrastructure builders are winning. Goldman, Morgan Stanley, Schwab, BlackRock, JPMorgan, and Carta did not acquire these platforms and data companies out of generosity. They acquired them because secondary transactions generate fees - management fees on fund products, commissions on marketplace trades, advisory fees on structured tender offers, data subscriptions on analytics platforms.

The more the secondary market grows, the more these institutions earn. Their incentives are aligned with market expansion regardless of whether the underlying assets perform.

The sophisticated sellers are also winning. Employees at SpaceX, OpenAI, and Anthropic who access company-led tender offers are getting liquidity at prices set by informed buyers in competitive processes. Early-stage VCs selling LP stakes in top-decile funds are getting fair value because the buyer pool now includes institutional secondary funds with $11.8 billion in dry powder. These are participants with information, leverage, and alternatives.

And this is, on balance, a good thing. The venture ecosystem has suffered for years from a liquidity bottleneck.

Companies are now staying private for a decade or more. Employees unable to access the value they helped create. Early investors locked into positions long past the point where portfolio management would dictate a sale. Secondaries relieve that pressure. They give founders an alternative to premature IPOs. They give employees real money instead of paper wealth.

They give early-stage VCs the ability to return capital to LPs without waiting for an exit that may be years away. More liquidity, flowing more freely, through more channels, is net positive for the health of the venture ecosystem.

Some institutional buyers on the secondary market are doing this well. They build diversified portfolios through disciplined entry-point selection while providing genuine liquidity to sellers who need it. Funds like Dave McClure’s Practical Venture Capital and OnePrime Capital are good examples: rigorous on price, systematic about portfolio construction, and performing a real economic function by giving sellers a bid when they need one. Informed buyers, willing sellers, fair prices, value creation on both sides. That is what a healthy secondary market looks like.

The problems can begin when this dynamic gets repackaged for a different audience. Are retail participants - the end buyers of PVC fund shares - winning too, or are they simply the last link in a chain that extracts value at every prior step?

Consider the path a secondary share takes before it reaches a retail investor through a PVC fund. A seller (often an insider with superior information) sells to a secondary buyer (often the PVC fund itself, paying a negotiated price), who packages it into a fund (adding management fees, performance fees, and operating expenses), which lists on a public exchange (where market dynamics can push the share price to a premium over the fund’s already-marked-up NAV). Each step adds cost. Each intermediary takes margin. The retail investor at the end of this chain is paying the cumulative markup of every participant who touched the asset before them, and is driven by brand recognition from fully priced assets.

This is not inherently predatory. Intermediation has costs, and access has value. The question is whether the total cost of that intermediation is proportionate to the access provided. When that underlying asset value is itself derived from secondary market prices that may reflect optimistic marks rather than realized exits, the effective premium to realizable value could be substantially higher.

The institutional channels opening up through Goldman’s Industry Ventures, Morgan Stanley’s EquityZen integration, Schwab’s Forge Global platform, Nasdaq Private Markets, and BlackRock’s Preqin-powered private markets intelligence offer a comparison worth examining.

These channels provide secondary venture exposure to HNW and institutional clients at or near NAV, with institutional governance, audited valuations, and transparent fee structures. They are not democratizing access - they are reserved for clients who meet wealth thresholds. But they demonstrate what fairly priced secondary access looks like. The gap between that price and the price a retail PVC investor pays is the cost of “democratization,” and investors should know exactly what that cost is before they celebrate being invited to the table.

The structural shift in venture secondaries is real and durable. A $106 billion market that functions at both ends of the cycle is not going away. But structural shifts are morally neutral. What matters is not the existence of the shift but the terms on which different participants access it, and whether the people bearing the most risk are the ones with the least information.

A Better Model

There is a different model. BlackRock acquired Preqin for its breadth - fund performance benchmarks, LP data, deal flow aggregation across all private market asset classes. It is a horizontal data play. But Preqin’s venture coverage is, by design, retrospective. It tells you how funds performed, not which companies will perform. It catalogs the past.

A data platform that does something Preqin cannot would have future predictive potential. It would score each private venture backed company in real time, based on the quality, concentration, and track record of their early-stage backers. That is not a database of what happened. It is a predictive filter for what is likely to happen - a quantitative signal that identifies which companies, at the moment they reach scale, have the backer profiles most correlated with outlier outcomes.

The difference between cataloging 100,000 private companies and algorithmically identifying the top decile at a specific inflection point is the difference between a library and a lens.

This matters for the secondary market because the core problem PitchBook’s data reveals - 86% concentration in 20 names, information asymmetry favoring insiders, retail investors at the end of the markup chain - is fundamentally a selection problem. Most participants in the secondary market are buying names they recognize. A systematic scoring model that evaluates every company against the same quantitative criteria offers something the secondary market currently lacks: a basis for selection that is neither brand-driven nor insider-dependent.

The infrastructure build in venture secondaries is being fought on four layers: transaction execution, data and benchmarking, distribution, and selection/access. The first three are increasingly dominated by the largest financial institutions in the world. The fourth - the ability to systematically distinguish which companies have the highest probability of outlier outcomes and access them early - remains open.

In a $106 billion market where 86% of volume chases the same 20 names, the investors who can identify the next 20 before they become consensus will capture most of the value. Everyone else is paying for the privilege of arriving last.

Keith Teare is founder and CEO of SignalRank Corporation. This analysis is based on PitchBook’s 2025 Annual US VC Secondary Market Watch (published February 20, 2026) and reflects his views on the venture secondary market. It should not be construed as investment advice.