The rise of retail in public & private markets

Retail capital is playing an increasingly important role in public & private markets alike.

The FT pointed to this chart (Figure 1) to show that retail now represents 20%+ of trading volumes in the US public markets, back to % levels not seen since the 1980s.

Figure 1. Retail share of US trading volume

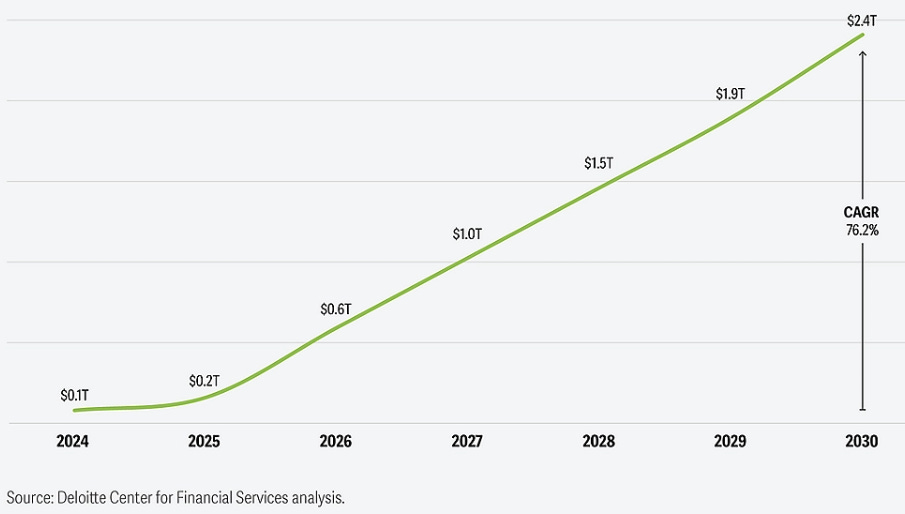

Similarly, the AUM for retail assets in the private markets is expected to scale rapidly. Deloitte anticipates exponential growth ahead, with $2.4 trillion allocated by US retail investors in private assets by 2030 (Figure 2).

Figure 2. US retail allocation to private capital to 2030 (AUM, $ trillions)

US policymakers seeking to open up 401(k)s to crypto and private markets alike will certainly help in achieving these numbers. This trend does have some echoes with history. To use the modern parlance, the “democratization of credit” helped fuel a speculative frenzy in the 1920s. Will the “democratization of alternatives” have a similar impact?

Institutional actors are paying attention. The ILPA warned its members that retail vehicles have distinct governance and regulatory requirements from institutional funds, as well differences in liquidity, valuations, fees and transparency. Similarly, Moody’s argues that selling funds to retail introduces new risks to GPs including “reputation loss, heightened regulatory scrutiny and higher costs” and potentially “systemic consequences.”

Nevertheless, the key point is that retail will be competing with institutional LPs for allocation into the same underlying companies.

This is most visible today in the pre-IPO companies (especially with the launch of the new Public Venture Capital models like Robinhood & Destiny).

Subject to regulatory considerations and appropriate structuring, SignalRank intends to explore making elements of its Series B strategy available to a broader investor base.

More broadly, we anticipate retail vehicles to deploy capital at earlier stages in the capital stack than has historically been the case.